Let us help you achieve greater and more profitable growth. Click here.

If you are thinking your response to what is happening around Open Banking, this will provide you with some valuable historical context on how events evolved to get us where we are today:

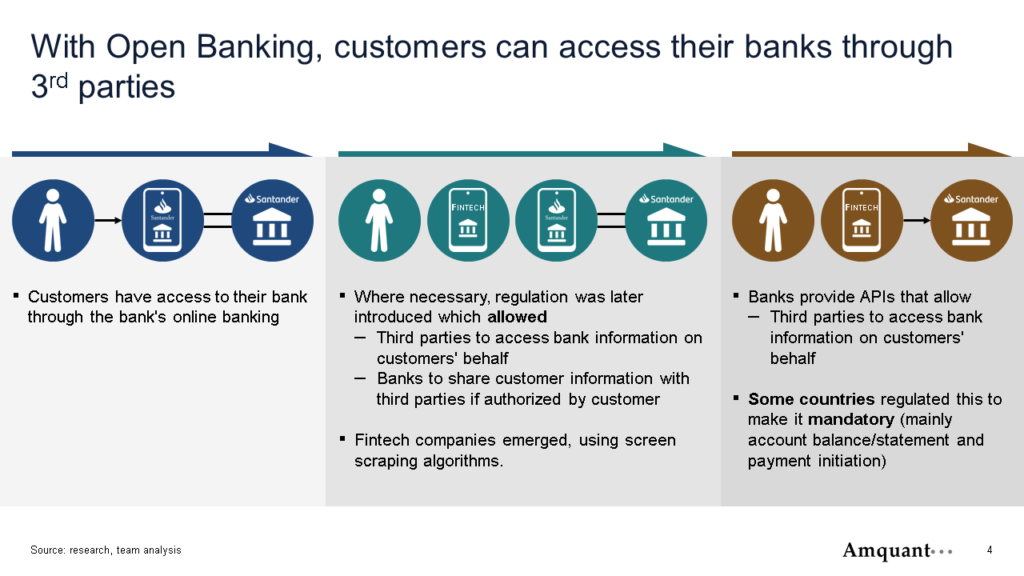

It all started with online banking.

Before Open Banking, banks thought it would be a good idea to give their clients access to their accounts using the internet.

So, since clients could access their accounts using online banking – some start-ups realized that if these customers provided them with their bank login information, they could log in on these accounts and manage them on their behalf.

Also, at that time, legislation was evolving.

In most of the World, there is customer data that banks cannot share, even if authorized by the customer. For example, credit data.

However, in recent years, if, on the one hand, you see a tightening in data privacy protection, on the other hand, you also see the relaxation and regulation of financial data sharing.

These two factors – the spreading and deepening of online banking and the regulation of financial data sharing, beget a whole generation of fintechs.

These start-ups had algorithms that logged in your account, copied the information displayed on the screen, interpreted that information and used this data to populate their database to provide you with their services.

However, this process has several obvious limitations:

- it is prone to errors,

- algorithms need to be updated every time a bank makes changes to their online bank,

- it is slow,

- it is a security risk,

- it is limited on what it can do,

- it requires a whole lot of trust.

So, banks started to provide access to client data and functionality via more official and stable ways. APIs have emerged as the winning solution. APIs allow third parties to use data without storing it and to access bank functionalities.

Hence, banks started developing and publishing APIS that allowed third parties to check balances, initiate transfers, etc.

Note that the emergence of APIs catalyzed many changes in how banks share data and functionalities beyond Open Banking. For example, there are three types of APIs:

- Public APIs, which TPPs use and are the most relevant for open banking,

- Partner APIs, which specific businesses use (e.g., buyers and vendors) to exchange data, and

- Internal APIs, which are proprietary and used to share data and functionalities within an organization.

Since 2018, some countries like the UK have started mandating all banks to provide and maintain specific APIs – typically account balance & statements and payment initiation instructions.

Most of these countries also introduced mechanisms to resolve disputes, service level requirements, and a centralized registry of companies authorized to use public APIs on behalf of their clients.

However, even in countries without this mandate – like the US, banks started to see this as an opportunity to become more agile and create new businesses. They started providing APIs voluntarily, enriching the data and functionality of these APIs (e.g., quotes, branch location, etc.) and cultivating the developer community to increase usage and loyalty.

This proliferation of APIs propelled the growth of another type of provider: the intermediaries.

These companies, which often also provide a platform for banks to develop, publish and manage their APIs, started providing Fintechs with a single, compliant, and unified point of access – thus eliminating the need to build, reconcile and maintain individual connections to multiple banks.

Today, it seems that these intermediaries have positioned themselves to either compete on scale (connection to the largest number of banks) or on value (specialization on specific uses or products).

It also seems that there is a lot of interest in replicating the success of Open Banking in other sectors like insurance, investment, wealth, and finance.

– – –

Even though I presented them sequentially (since certain events and factors kickstarted other events and factors), all these things can be found co-existing today. For example, it is estimated that about 4 million Canadians (one in every seven) currently use a screen scraping app.

The reality is that the timeframe of these events is painfully compressed. The UK – the pioneer in Open Banking – introduced its legislation three years ago. Plaid (now a US $15 billion intermediary recently targeted for acquisition by VISA) was founded less than a decade ago.

If you do not have a strategic response to this trend now, you cannot afford to wait.