Let us help you achieve greater and more profitable growth. Click here.

If you are a bank executive and want to manage the bank’s business strategically, you must understand the key drivers of your bank’s profitability and the trade-offs they imply.

For example, to some extent, banks can trade the cost of deposits for efficiency ratio by making it more convenient for clients to make deposits.

At the same time, the equilibrium of these trade-offs depends on a number of external factors which change all the time. In our example, while the status of the labor market impacts banks’ efficiency ratio, the compression of interest rates impacts the attractiveness of low-cost deposits.

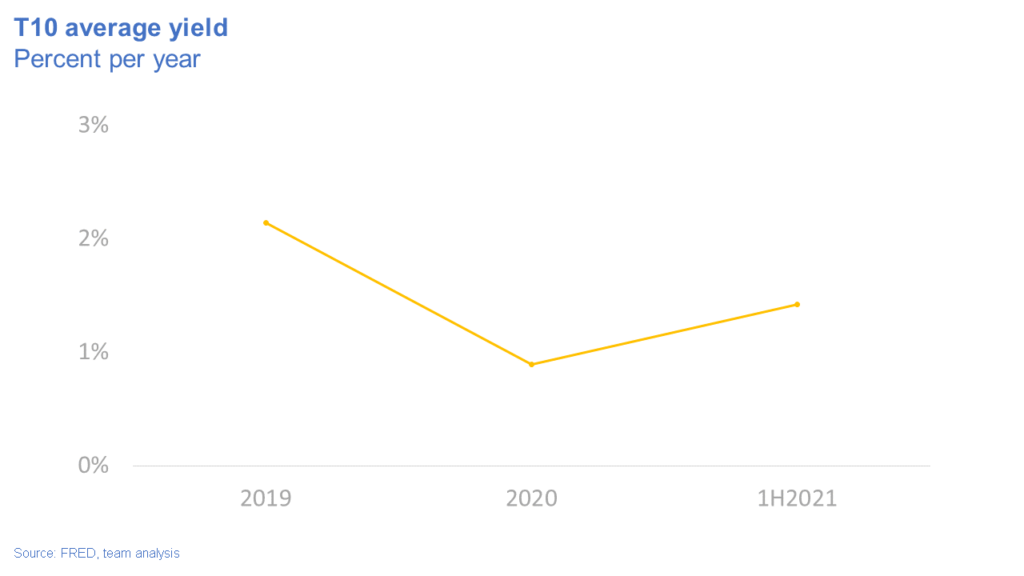

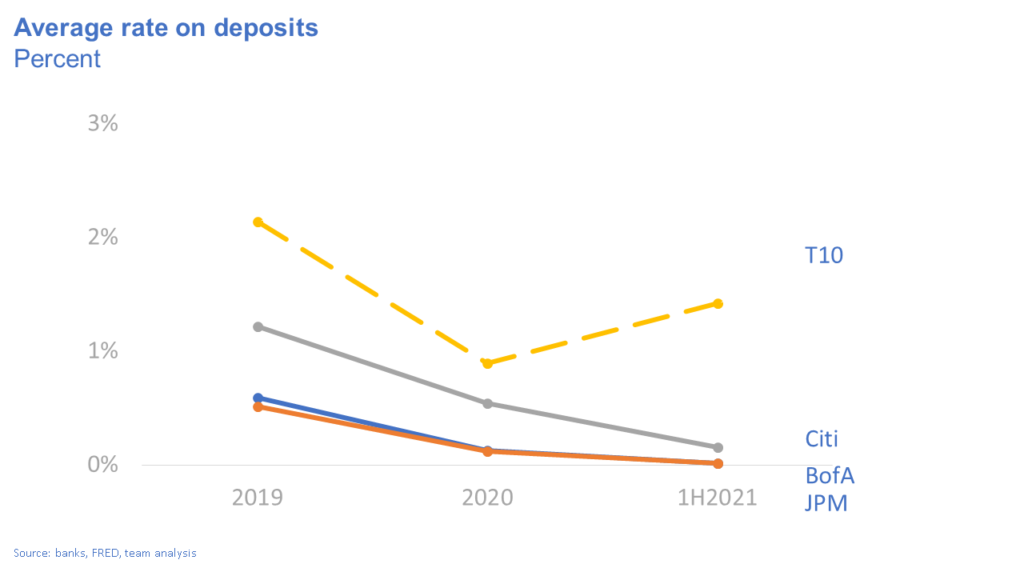

Take interest rates for example. In 2019 10YTs paid on average 2.14%. They then fell to 0.89% in 2020 (a 125 bps reduction) and up to 1.42% in 2021 (a 53 bps increase).

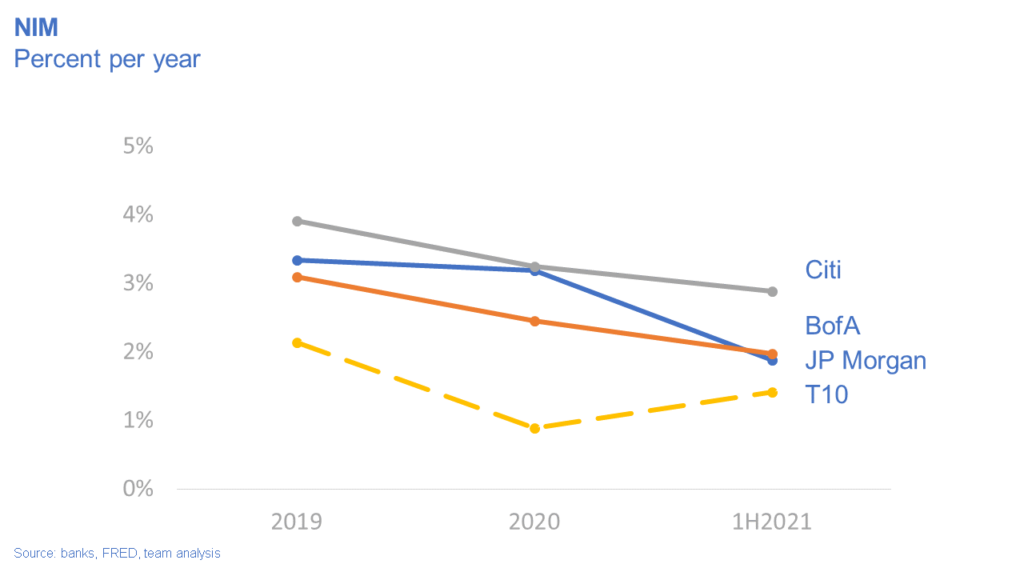

How the large banks’ NIM were impacted and how they responded to this?

The NIM of JP Morgan, Bank of America, and Citibank have been decreasing, having lost between one and one and a half percentage points in the same period. To put this in perspective, my rule of thumb is that banks need around one percentage point of NIM just to pay their cost of equity to hold banking assets, which is not accounted for in the NIM formula.

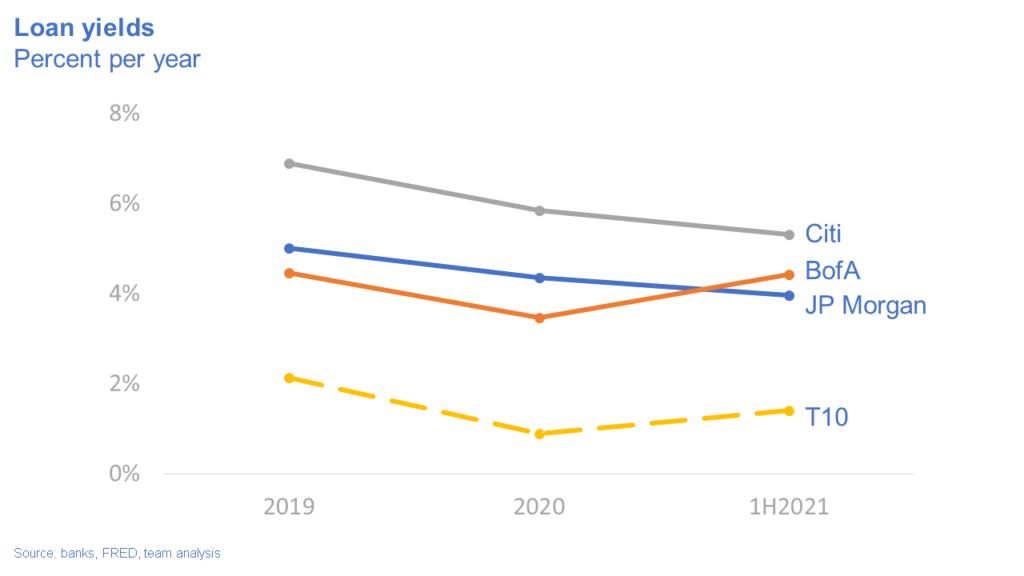

Loan yields have been significant drivers of this reduction – kind of. Take for example Bank of America. The bank’s NIM decreased by more than one percentage point even though its loan yield is now close to its 2019 level. The other two banks’ NIMs have also not mimicked the changes of their loan portfolio’s yield.

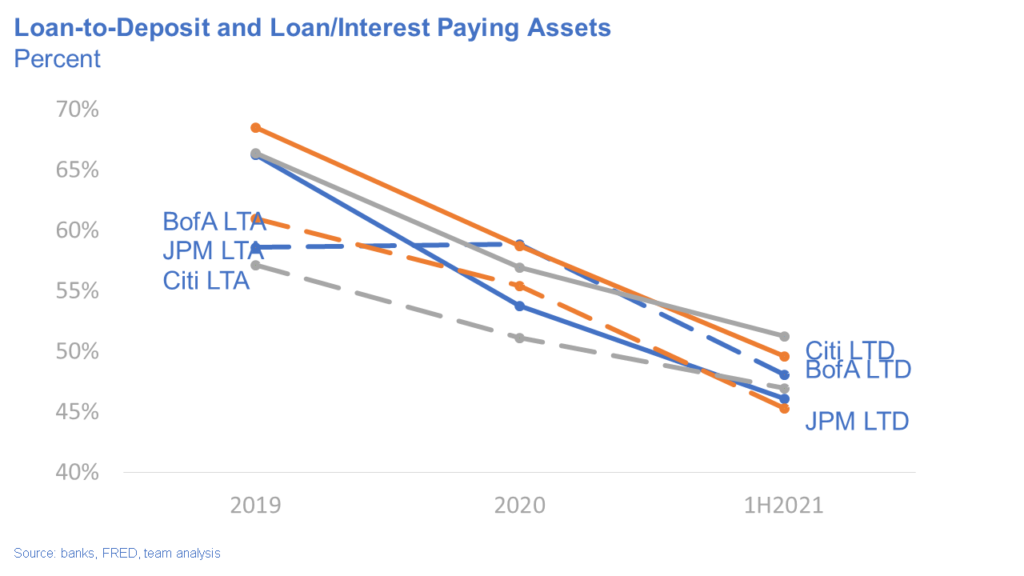

One not obvious driver has been the reduction of the loan portfolio, both as a percentage of total interest-earning assets as well as a percentage of deposits. We estimate that, if loans have grown at a similar rate as deposits and total interest-earning assets, this would have added an extra thirty basis points to these banks’ NIMs.

The role of deposits changes. For example, the cost of non-interest-paying deposits does not change with interest rates. Therefore as interest rates decrease, those deposits slow down the decrease of the cost of NIM.

For you, some implications of this landscape include:

- As NIM continue to inch down, you should rethink the strategic value of their banking business and how much operating cost they put behind originating loans and deposits.

- Since higher yields are accompanies by higher risk, your footprint and risk management will continue to differentiate the results from your loan portfolio.

- In a scenario in which abundance of liquidity and factors related to COVID depress the relative growth of loans, you should manage the utilization of your balance sheet.

- Rethink the strategic value of your deposits. Deposits have other strategic values in areas like liquidity, non-interest revenues and brand.